Zurich opens new bicycle tunnel

Tunnels can be used for all sorts of fun purposes. You could, for example, build one under a major urban highway in an attempt to relieve traffic congestion.

Alternatively, you could build a tunnel for bicycles; one that stitches together two disconnected parts of a city and creates a new modern parking facility for 1,240 bicycles. And on May 22, Zurich unveiled exactly this.

Here's a video (I have no idea what the guy is saying but hopefully it's positive).

21

21

The new tunnel — called the Stadttunnell — is only 440 meters long. But it runs under Zurich's main train station and connects District 4 and 5. Previously, this was a more awkward and dangerous connection given the train station.

What's also interesting about this tunnel is that it was started in the 1980s as part of a planned urban highway. But when that was scrapped, the tunnel sat dormant. Now it's back and it shows a massive commitment to sustainable mobility. The project cost 38.6 million Swiss francs.

I'd love to check in a year from now to see how well used it is, and how many people park their bikes here. Thankfully, there's a bike counter.

Cover photo from Stadt Zürich

You just need to get into the market

I have vivid memories of being in a broker meeting many years ago talking about development land in Vancouver. Our team's comment was that it felt expensive. I mean, Toronto was expensive, and Vancouver was even more. Why? It has one-third the GDP of Toronto. The response we got was something like this: "Yeah, Vancouver may seem pricy, but you just need to get into the market. Then in 5 years you'll be happy you did."

Well it's been more than 5 years and now this is the market:

The market for development sites is being tested by a roughly 50-per-cent drop in value since 2022, according to Mark Goodman. The principal of Goodman Commercial Inc. said Broadway Plan sites, for example, were selling for about $200 per square foot buildable three years ago. Sellers can now expect closer to $100 per square foot buildable, he told BIV. Goodman currently has three Broadway Plan listings.

Of course, Toronto is in a similar situation today. If there's no market for new condominiums and apartment rents aren't growing, then high-density land values are going to feel the impact. But I do think it's interesting that, in some ways, our response was being anchored by our experience in Toronto. What we know, and have accepted, often becomes a baseline for assessing if something else feels expensive or cheap.

I sometimes see the same thing with long-time developers. They remember what they used to sell and/or rent apartments for, and have a harder time accepting today. But this is a positive thing if it compels greater deal scrutiny. Advice like "you just need to get into the market" is never sound. But if you were to take this approach, I would bet that today is a better time than 5 years ago.

Don't make me search — just tell me the answer

Google is well aware that traditional search is going to die (or at least go away for the vast majority of use cases). I don't want to search for things if I can just be told the answer.

Here's an example. I was installing new light fixtures in our bedrooms this week and I wanted a refresher on wire colors.

Historically, I would have done a Google Search, which would have then led me to some website or to some lengthy YouTube video that I didn't actually want to watch and that I would have had to scan through to find the salient parts.

But today that feels old school. Instead what I did was take a picture of the ceiling box and ask ChatGPT to just tell me the answers.

Voilà:

It seems almost trite at this point to talk about the virtues of AI. But over the last few months, I have found that — just like that — it has become an integral part of my everyday workflow.

This is true whether I'm playing electrician, planning travel, writing a blog post (and I want an assistant to find me data), or I'm looking to brainstorm around something business related.

I'm sure the same is true for many of you as well.

How far do you drive each day?

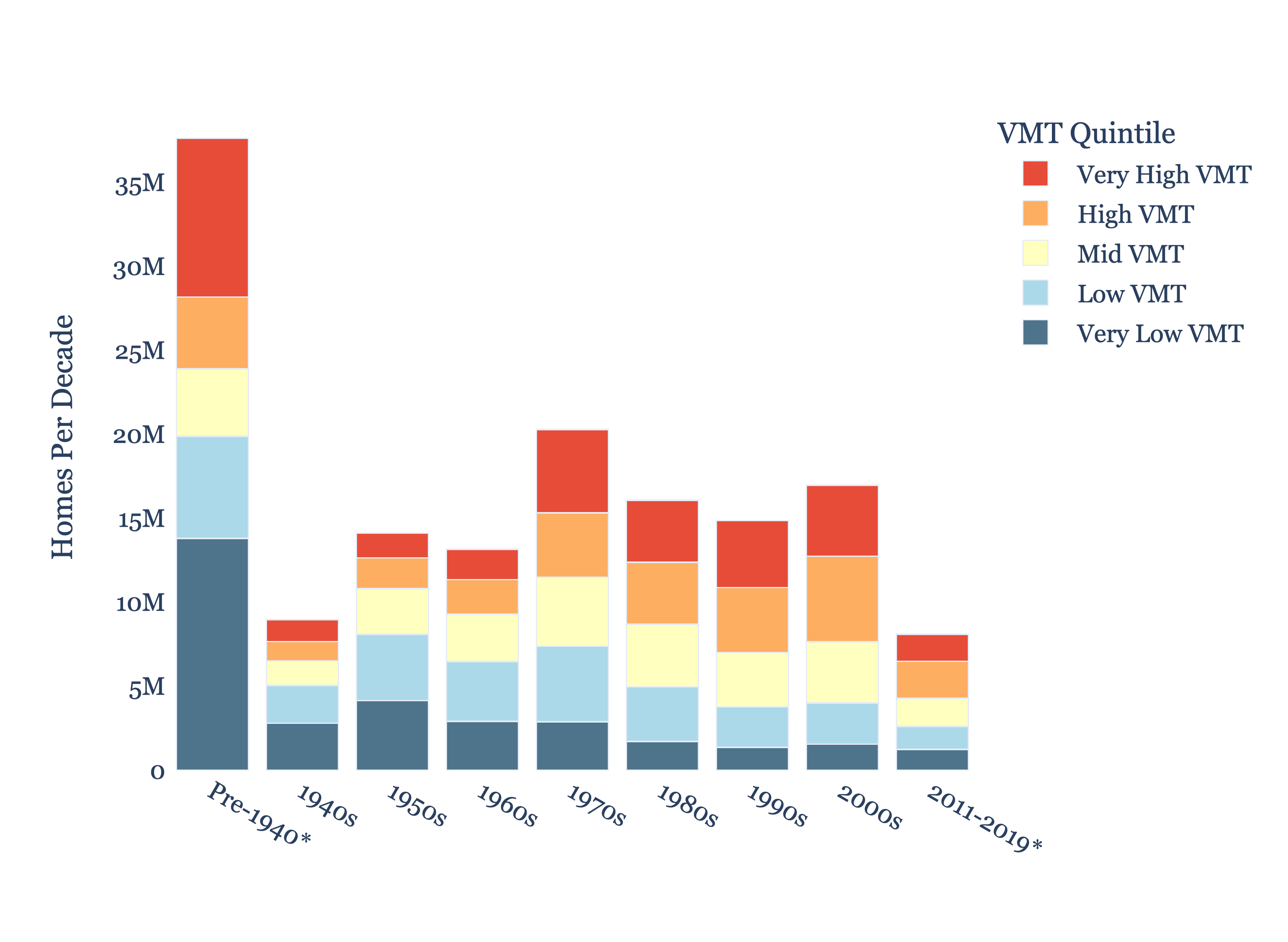

Sprawl is how much of the US provides new housing, and so it's interesting to ask the opposite question: Which cities are actually building new housing in walkable neighborhoods? Here is a study published this week by the Terner Center for Housing Innovation at UC Berkeley that looked at exactly this. What they did was divide all US neighborhoods into five categories based on vehicle miles traveled (VMT) per resident in 2023.

The categories:

Very Low VMT - 12 miles per person per day

Low VMT - 17.3 miles per person per day

Mid VMT - 21 miles per person per day

High VMT - 25.5 miles per person per day

Very High VMT - 37.5 miles per person day

These seem like oddly specific distances, but it's what they used to sort new housing supply. Here's all of the US:

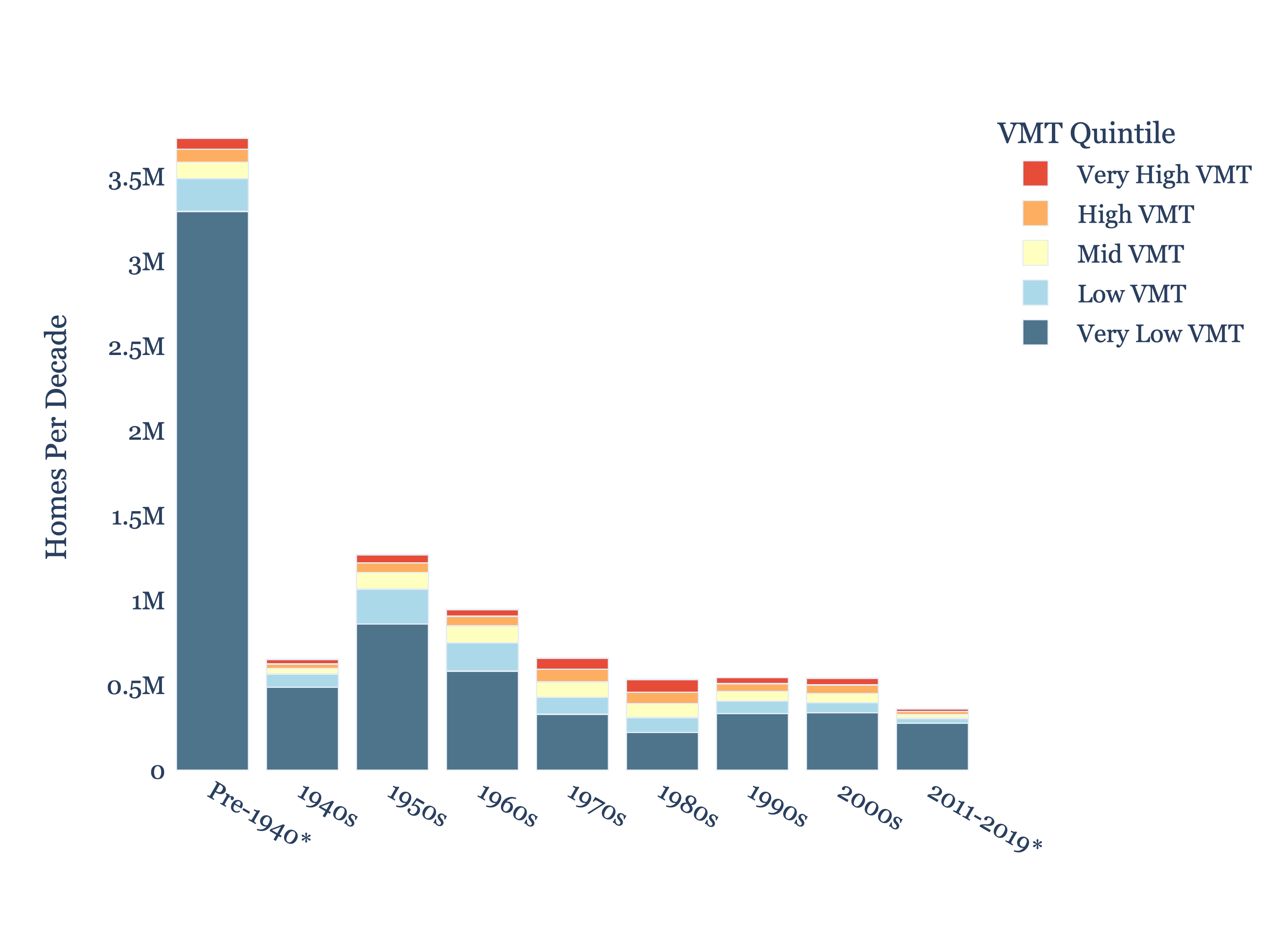

Since the 1950s, new home production in very low VMT neighborhoods has generally been declining. Most of the lower VMT stuff was built before the 1940s, which is why New York City is so walkable and its chart looks like this:

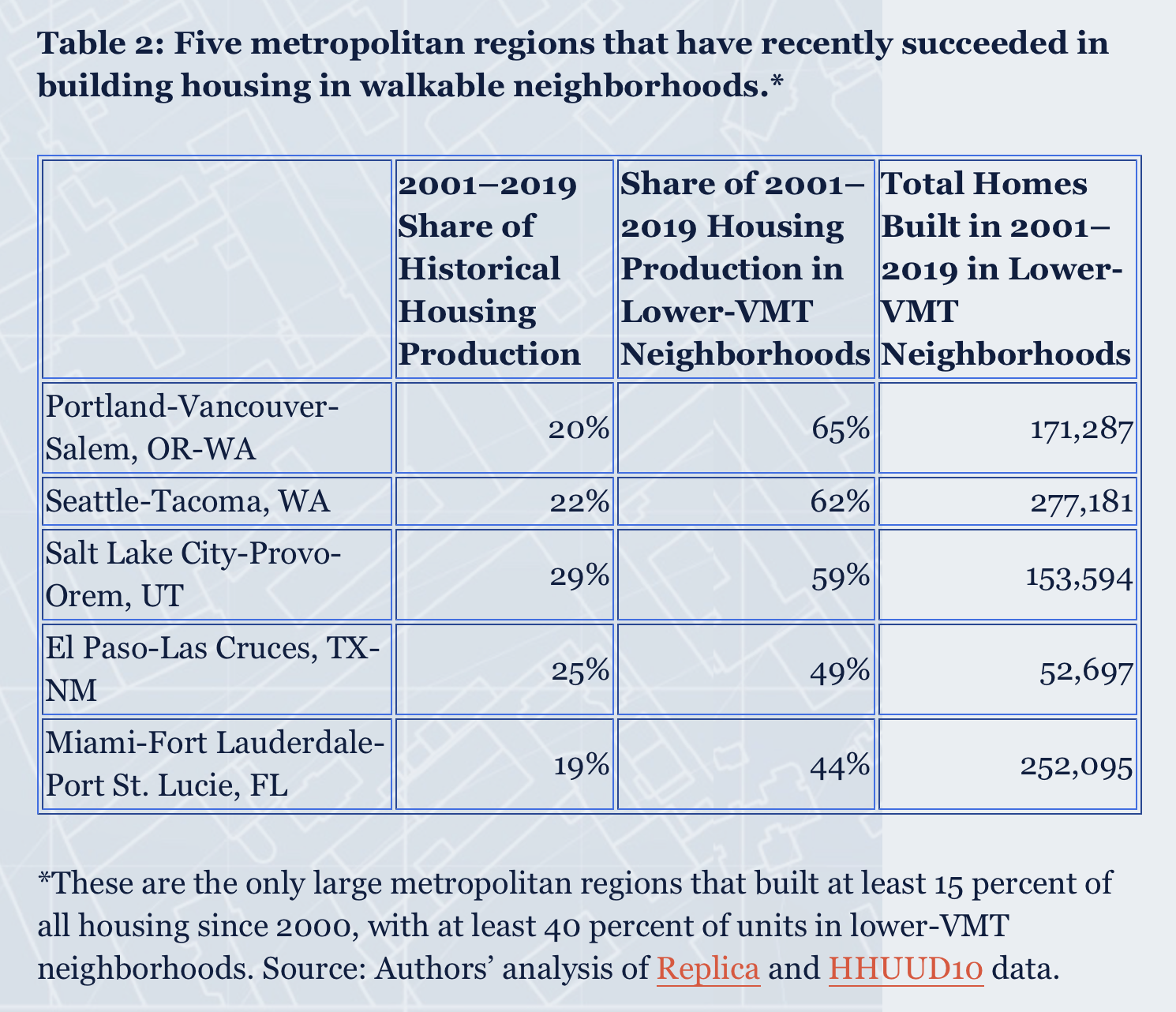

Most newer cities do not build in this way. In fact, based on this study, there are only five large metro areas in the US that have (1) built at least 15% of their total housing since 2000 (meaning, they're a younger city) and (2) built at least 40% of their homes over the last decade in lower-VMT neighborhoods (very low and low).

These metro regions are:

This is not that many cities. At the same time, is it even the right benchmark to be aspiring to? "Lower VMT" just means you don't need to drive as much as you might in other neighborhoods. But it doesn't necessarily mean that you live in an amenity-rich and walkable community. What about the new homes being built in neighborhoods where people don't need a car at all? How many of these exist?

Very few, I'm sure.

Cover photo by Jo Heubeck & Domi Pfenninger on Unsplash

Canada has $2.42 trillion of residential real estate debt

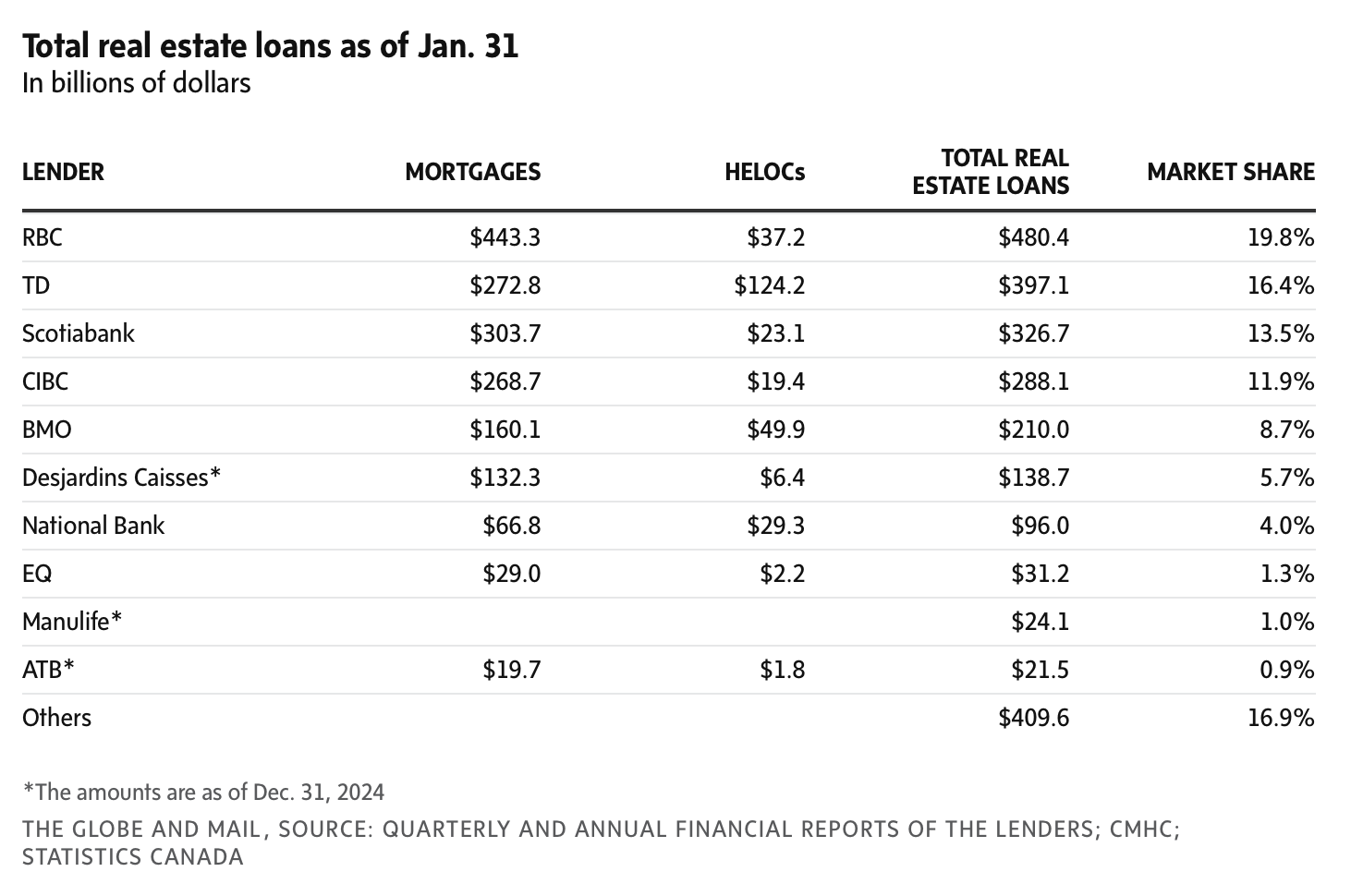

Here's an interesting table via the Globe and Mail:

As of January of this year, residential real estate loans in Canada totalled approximately $2.07 trillion. On top of this there's another $350 billion in home equity lines of credit. This brings total loans secured by residential real estate in this country to about $2.42 trillion.

What this chart really shows, though, is how concentrated the mortgage market is. The "big six" banks make up about 74% of the market. If you include Desjardins, the total increases to 80%. That's pretty much the market.

Cover photo by Tiago Rodrigues on Unsplash

I want to be a digital nomad

In my opinion, digital nomadism is a growing trend for at least two reasons: 1) people like traveling (it's more fun than sitting in an office cubicle) and 2) technology keeps making it easier to work in a decentralized way.

This is not a new phenomenon, but it's a growing one. In 2020, it was estimated that there were ~11 million so-called digital nomads in the world. This year it's somewhere around 40 million people. And it's hard to imagine this trend reversing.

Let's consider what's happening on the technology side. This week at Google I/O, the company announced a lot of AI-powered tech in the hopes of not becoming extinct as a result of it. And one of these things was a new 3D video communication platform called Google Beam.

Two things are really neat about this tool. One, it uses some AI volumetric video model to make the person in front of you appear in full 3D. So it's closer to real life. And two, it does real-time language translations. Here's a video of it in action:

In watching this, my mind immediately went to "this is going to make it even easier for people to work from Bogotá." It also collapses the world. Now we can all speak to each other regardless of language.

Imagine, for example, being able to participate in a community meeting for a new development project in Bogotá. You could be at home speaking in English and the community could be yelling at you in Spanish. That's powerful.

There's also speculation that Apple will be adding real-time translations to its AirPods later this year. Meaning, you won't need to hide behind layers of screens and technologies. You'll be able to get yelled at in person!

All of these innovations are only going to make it easier for people to live and work fluidly around the world. And I strongly believe that an increasing number of people will take advantage of it. But now the hard part: What does this mean for cities, real estate, and everything else?

Cover photo by Random Institute on Unsplash

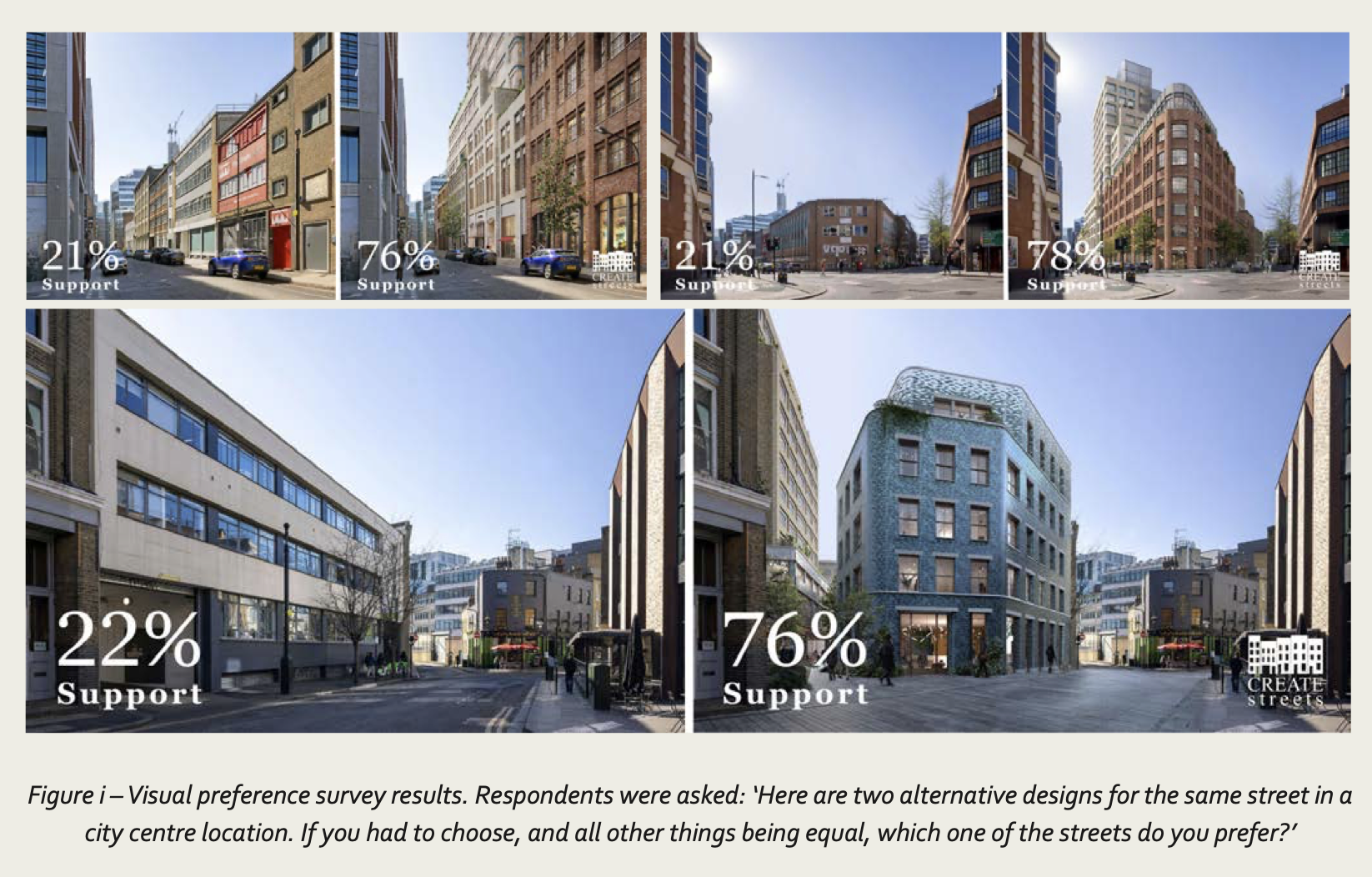

Visual preference survey

Create Streets recently published this review of the proposed Shoreditch Works development project in Hackney, London. And one of the interesting things they did as part of it was something they call a visual preference survey. What this means is that they showed a statistically representative sampling of over two thousand British people some before and after images so they could choose which they prefer.

Here's how they responded:

As you can see, from a visual perspective, there was/is strong support for the proposed development. At least according to these three views. This is despite the fact that the proposal is, of course, taller than what's there today. What I think this starts to show is that good design matters. People respond positively to beauty. And, that it's important to show what will happen at street level above all. This is how we all experience cities.

Visual preference surveys aren't all that common. I'm not sure I've seen one conducted for a new development. But it's a great idea and I plan to borrow it from Create Streets.

Cover photo from Shoreditch Works

Winter cycling capital of the world

Okay, so we know that Paris has transformed itself from a car city into a biking city. Between 2015-2020 the City doubled its number of bike lanes. Then in 2021, it announced that it wanted to become a "100% cycling city" and further add to its bike network. Today, it has one of the busiest bike routes in the world and more people cycle than drive. The Globe and Mail reported, here, that last year 11.2% of trips in Paris proper were made by bike, compared to only 4.3% by car. "You would not be wrong to call it a war on the car," Marcus Gee writes. However, the result was a "victory for the city."

At the same time, we know how people will respond to this data. Lots of people will read this article and immediately say, "yeah, but that's Paris, where the average highs and lows in January are 8 and 3 degrees, respectively. It simply won't work in Toronto where our January highs and lows average 0 and -7 degrees. We have snow to contend with; they don't." And of course, they wouldn't be entirely wrong in this argument. Cycling does tend to decline in the winter months in most cities. (Note: The months of April to November in Toronto are just as warm or warmer than Paris in the winter.)

But just for fun, let's look at Oulu, Finland which has been called the "winter cycling capital of the world." Oulu has a population of around 210,000 people, an extremely low population density of approximately 150 people per km2, and January temperatures that average between -7 and -15 degrees. And yet: 40% of residents report cycling on a weekly basis, more than 40% of trips to school are by bike, 22% of all trips in the inner city are by bicycle, and this number remains at 12% throughout the winter. These Oululainens are clearly hardy people.

Here's a video comparing winter vs. summer cycling in Oulu.

I'll be the first to admit that I don't generally cycle in January and February. Partially because it's cold and partially because I don't want road salts all over my business. But the correct framing isn't that it's not possible in a city like Toronto; it's that I'm too soft. That, and we need to invest in the right infrastructure if we want more people to do it.

The city is the amenity

The City of Toronto requires amenity spaces to be provided in new housing developments of a certain size. Here, for example, is the relevant excerpt from the recommended zoning by-law amendment that is expected to allow small-scale apartments along all major streets:

The triggers are 20 and 30 dwelling units, which represents a housing scale that Toronto doesn't build a lot of. I mean there's a reason it's called the missing middle. That is, of course, the point of the major streets study. It's to build more of it. But for that to happen, these amenity requirements have got to go.

Firstly, because it's not feasible at this scale. Think of it this way: two square meters of indoor amenity space x 20 dwelling units = 40 square meters of indoor amenity space or ~430 square feet. Multiply this by an average rent of $5 psf (and then 12 months) and that's nearly $26k of foregone revenue for the project.

This may not seem like a big number for a development project, but consider that at an NOI margin of 77% (i.e. if you deduct operating expenses), this revenue number works out to a net operating income of just over $20k. Capitalize this at 4% and you've just removed $500k of value from the project.

Another way to look at this would be to divide the $26k of foregone rental revenue by the 20 dwelling units. This works out to nearly $1,300 of annual revenue per suite — revenue that will then need to be made up by everyone who lives in the building.

The second reason why I think this requirement needs to go is because it's a suburban way of thinking. In the suburbs, people tend have their own backyards. And so the logic goes that in multi-family buildings, people should also have their own private (albeit shared) amenities.

That's fine if it makes sense for the project. But we shouldn't forget that the reason cities are so wonderful is that they are rich in amenities, culture, and the myriad of other things made possible by collective contribution. World-class museums and galleries, for instance, almost always require big city resources to be viable.

On some level, I think you could argue that there's an irony to this planning requirement. We mandate amenity spaces because amenities are of course good. But it hurts project feasibility, especially at smaller scales, which then limits the amount of new homes, density, and people we have in our existing neighborhoods.

And because we are limiting density, we are indirectly limiting the kind of private and public amenities that might otherwise be feasible if only there were more humans to support them. So I would strongly encourage the city to rethink its position on required amenity areas. At the very least, the triggering unit counts should be raised.

For more on this topic, here's a recent article from the Globe and Mail by John Lorinc.

Photo by Filip Mishevski on Unsplash

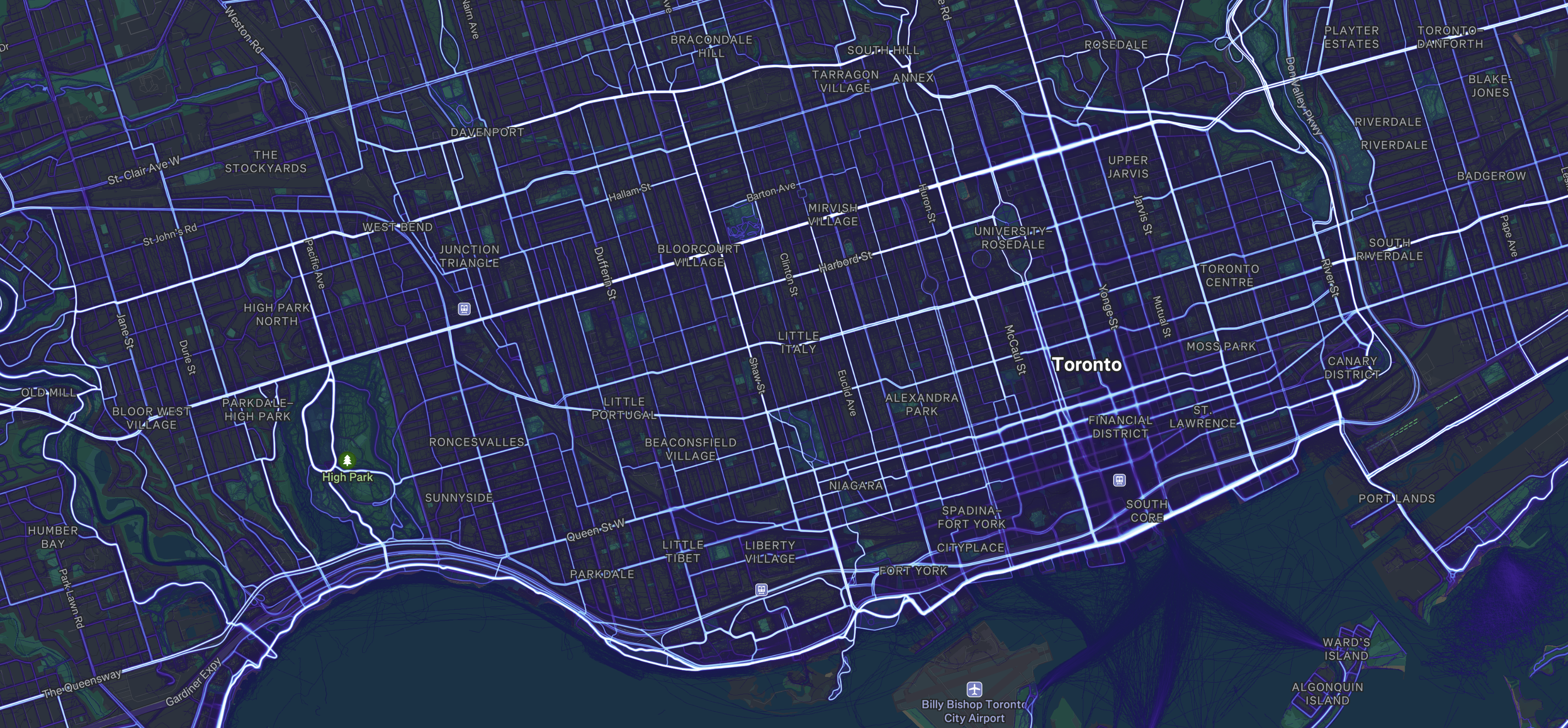

Strava's global cycling heatmap

Yesterday morning I went cycling in High Park to try and condition myself for the Bike for Brain Health ride that I have coming up. The Park is such an incredible amenity and I love being so close to it. Of course, before I set out, I turned on my Apple Watch and Garmin computer so that I could track it all in Strava. This has become such a big part of cycling (and working out in general). We're all data obsessed. Everyone wants to track their route, their speed, their heart rate, and whatever else.

The result is that Strava collects mountains of data about the way people actively move about in cities — data on everything from cycling to backcountry skiing. Some of this aggregated/anonymized data is available to the public via their global heatmap, but much more of it is available to urban planners and active transportation groups around the world. In fact, this is part of what Strava does: they help city builders. Here are some urban case studies spanning Rio de Janeiro to Park City.

Looking at central Toronto, our heatmap looks like this:

What is immediately noticeable is that cyclists will go where they feel safe. And that generally means streets with dedicated bike lanes. Looking at the above map, you can see that some of the most popular north-south routes are Shaw Street, Beverley Street/St. George Street, and Sherbourne Street. All of these streets have dedicated bike lanes. In the east-west direction, it's also clear that Bloor Street and Danforth Avenue form a hugely important crosstown artery. It is widely used from Etobicoke all the way to Scarborough.

At the same time, these maps start to show where there are broken links in the network. Annette Street and a portion of Dupont Street are, for example, widely used until you get east of the Junction Triangle. Then it falls off. This is unsurprising because it's a stretch of Dupont that isn't very friendly to cyclists. I know I certainly try and avoid it. Instead, we see that cyclists seem to be shifting northward to Davenport, which has a nice bike lane.

This is just one example, and I'm sure there's a lot of other takeaways that can be gleaned from Strava's data. So if you're a city builder and you aren't already leveraging this dataset, you may want to consider applying for a Metro Partnership. I'll be sure to continue doing my part and feeding it data about my laps in High Park and my stops for burgers and croissant sandwiches.